- Access to legal advice helpline

- Tax investigation cover

- Property disputes legal cover

Landlord Legal Expenses Insurance

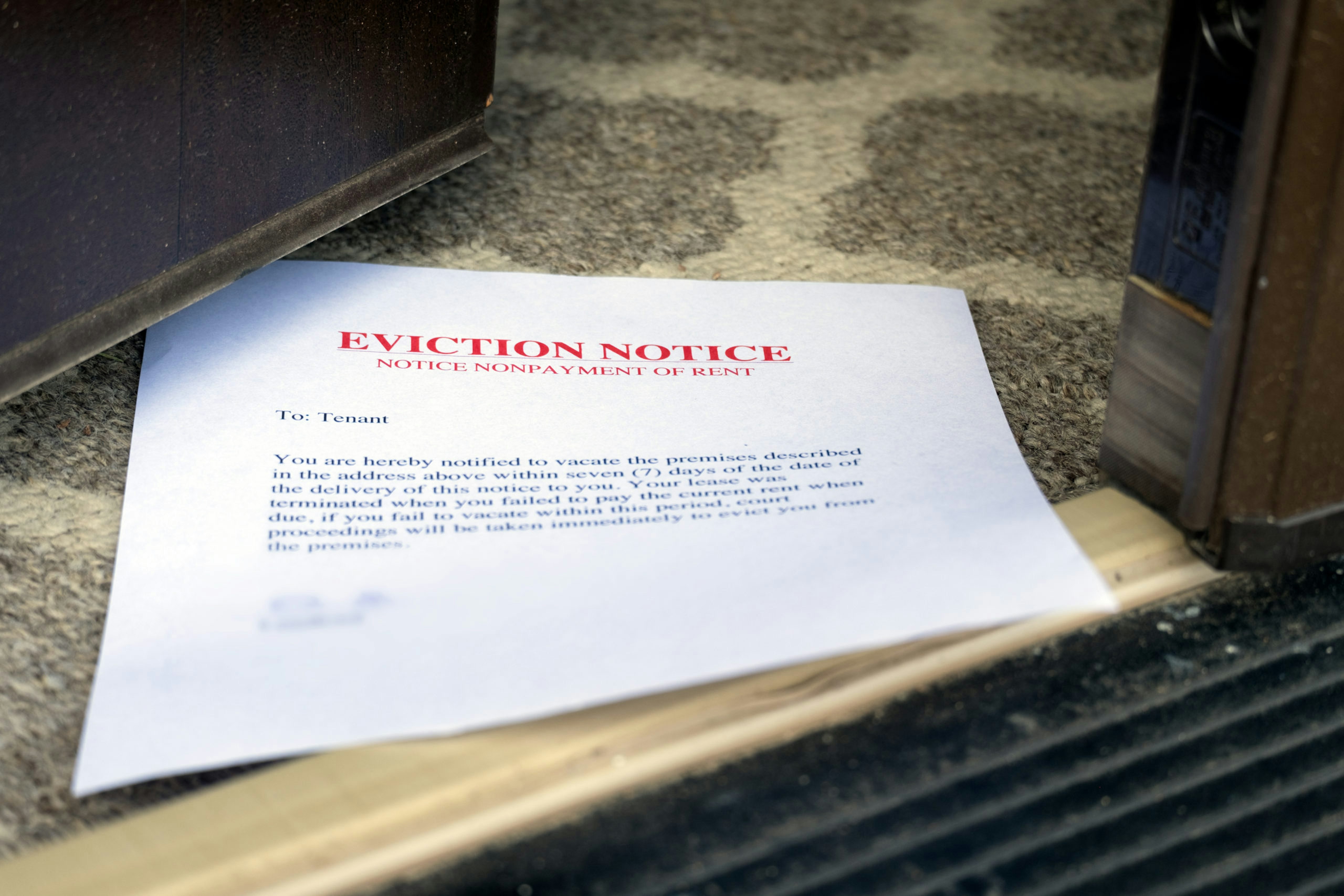

Covers landlord's legal costs for tenant disputes, evictions, and property damage claims, safeguarding you against high legal fees.

- From £60 a year per tenancy

- £100,000 legal expenses cover (including eviction costs)

Landlord legal expenses insurance provides legal advice and cover for legal costs should a dispute relating to your property and tenant(s) arise, such as legal action and court proceedings, up to £100,000. For example, you can benefit from having legal expenses insurance if a tenant damaged your property, if you need to evict your tenant(s), or if you wanted to seek unpaid rent.

Landlord legal expenses cover is essential for landlords who want to keep control of their property at all times. Usually tenancies run smoothly and there is little cause for concern, however, when it does go wrong there can be lengthy and costly legal disputes.

The Alan Boswell Group Difference

We appreciate that when you’re letting a property there needs to be a continuous income flow. If something jeopardises this income, action needs to be taken quickly. That’s why we have worked to develop landlord legal expenses cover; a product that covers the major legal issues a landlord could face and provides support so situations are remedied quickly and efficiently.

Our landlord advice hub is full of useful information to help landlords and property owners find the advice and products needed.

How our customers rate us

Landlord legal expenses insurance in detail

Eviction cover

General property disputes cover

Repair and renovations disputes cover

Health & safety prosecutions

Tax investigation cover

Rent recovery

Access to legal advice

Removal of squatters by interim possession order

Replacement of locks following legal eviction by bailiff or sheriff

Storage of tenant’s goods following legal eviction by bailiff or sheriff

If tenants already occupy the property and you wish to take out this policy midway through their tenancy there will be a 60 day exclusion period before any claim can be submitted.

FAQs

Get in touch

Whether you need a quote, have a general enquiry, want to register a claim, or talk it through over the phone, we're here to help.

Related products

Landlord building insurance is vital cover for your rental property. We can search the market, compare quotes, and arrange your insurance so you get the best cover available.

Commercial building insurance for landlords from a market-leading broker. We'll search the market and compare quotes so you can choose the best insurance.

Provides insurance for non-payment of rent in the event of a tenant defaulting, as well as any landlord legal expenses cover of up to £100,000.

A comprehensive flat insurance policy tailored to your requirements will give you peace of mind, talk to one of our specialists today or get a quote online

Landlord liability insurance keeps your tenants, or anyone employed to work on your property, safe.

Multi-property landlord insurance for your residential and/or commercial property portfolio.

Secure peace of mind with our comprehensive unoccupied property insurance, providing reliable cover to safeguard your investment and protect against unforeseen risks.

Related guides and insights

All you need to know about landlord legal expenses cover

At a time when tenant evictions are rising – and tenant powers to take their landlords to court are stronger than ever – landlord legal expenses cover is a must. We look at how it works and how you can get the right insurance.

How to remove squatters: a guide for residential and commercial landlords

Learn the legal steps to remove squatters from residential and commercial buildings, plus timelines, costs, insurance considerations, and prevention tips.

How to evict a tenant: a guide to the new rules

Section 21 ‘no-fault’ evictions no longer exist, which means you cannot evict a tenant because their tenancy term has ended, and the only eviction method is to issue a Section 8 notice. We explain the new rules and what that means in practice for landlords.

What is a no-fault eviction? A guide for landlords

The Government are set to abolish Section 21 ‘no-fault evictions’ in the coming months. We take a look at what this means for landlords, and the grounds they can still use to evict.