Your guide to the personal injury discount rate

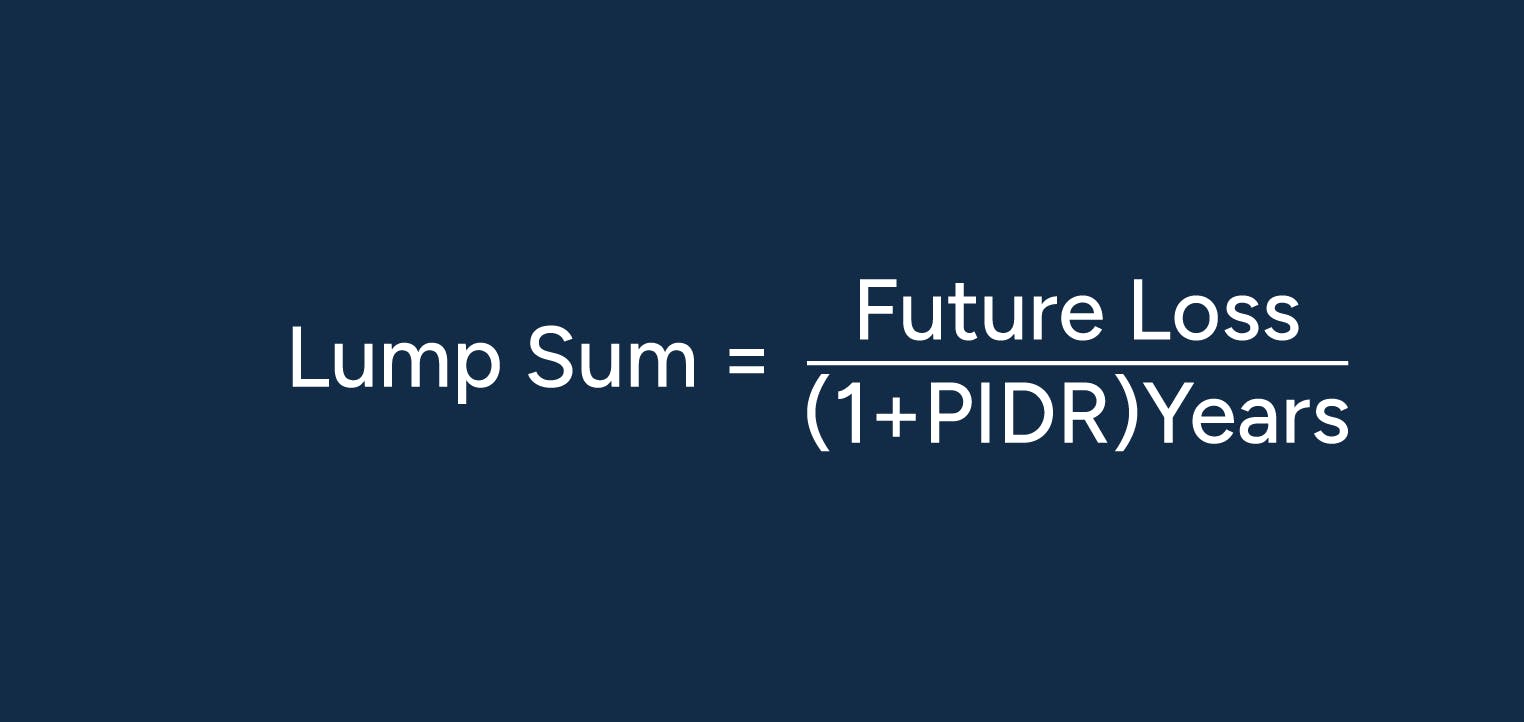

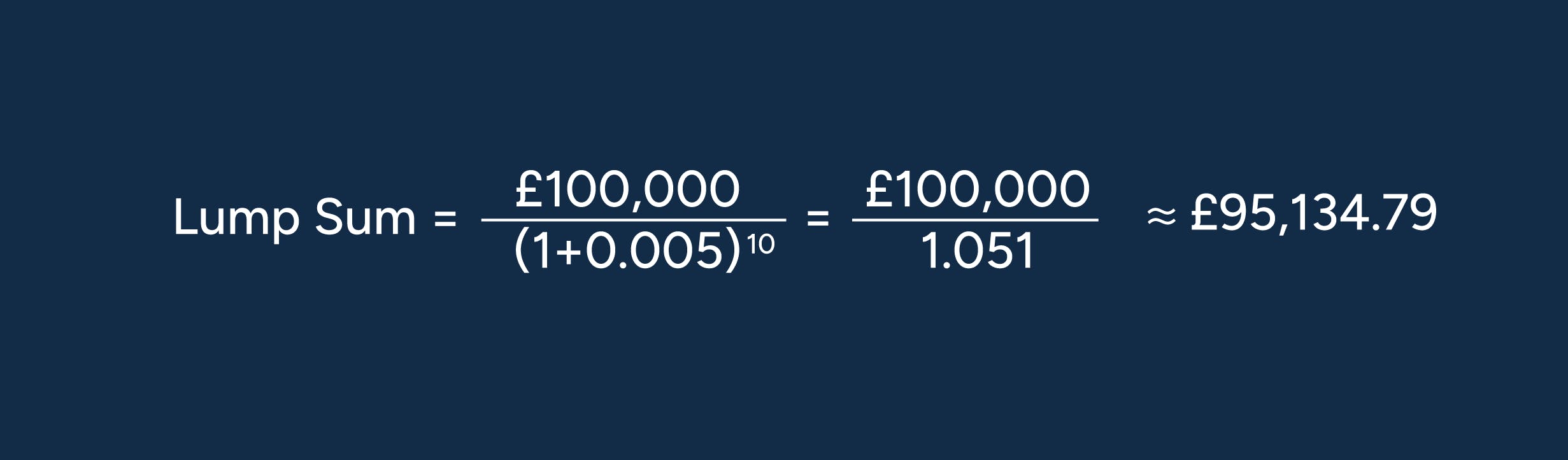

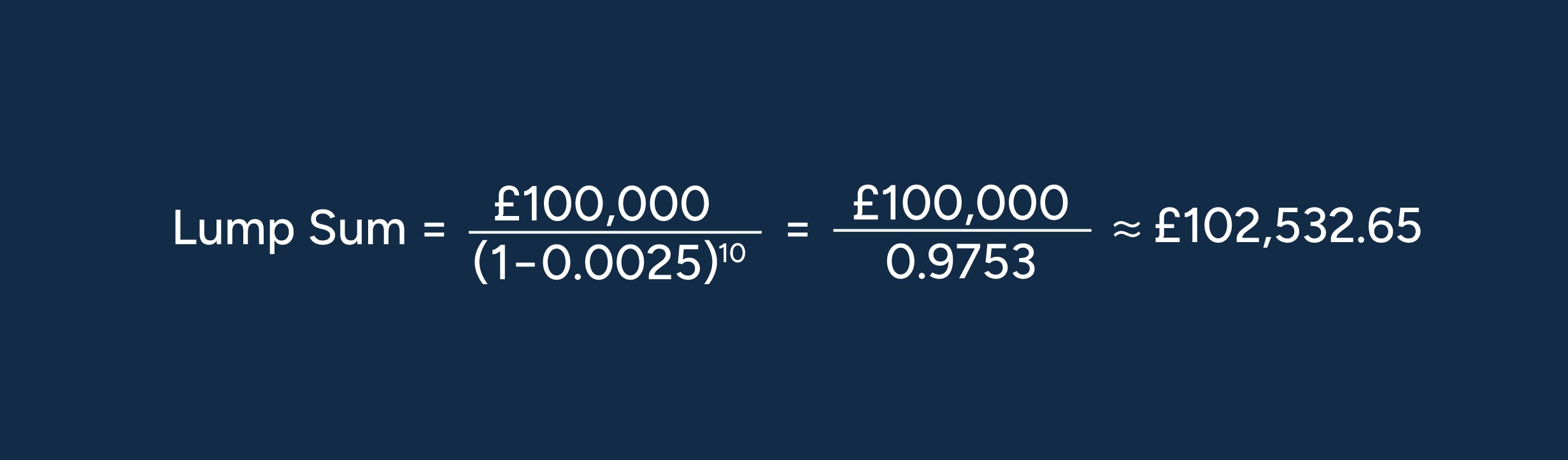

The Personal Injury Discount Rate (PIDR) is a figure used to adjust lump sum compensation payments for high-value personal injury and clinical negligence claims. This figure is set by the Lord Chancellor in England & Wales, and separately for Scotland and Northern Ireland by the Government Actuary.

04.01.22

By

![]() Tom Head

Tom Head

Related guides and insights

Public Liability vs Professional Indemnity insurance

One of the questions we’re most often asked is about the difference between public liability and professional indemnity insurance. In this article, we explain how these policies work.

Your guide to Public Liability insurance

We answer your commonly asked questions in our guide to Public Liability insurance, including what it is, who needs it and how much it typically costs.

A business guide to employment practices liability (EPL) insurance

Protect your business from the cost of rising UK tribunal claims. Learn how EPL insurance covers claims arising from unfair dismissal, discrimination, and modern remote working risks.

Guide to personal accident car insurance cover

Personal accident cover pays out compensation to you or your beneficiaries if you’re seriously injured or die in a car accident. It’s also known as personal injury insurance.